![]()

| Main index | Financial Markets index | About author |

![]()

Gilts mentioned | |||||||||||

| Name | Cpn | Maturity | Size £m |

Gov’t £m |

BoE £m |

S-G-B £m |

← ÷S |

When issued |

Orig. term |

S? | ISIN |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 4T20 | 4.75 | 07 Mar 2020 | 32,954 | 4,941 | 14,500 | 13,513 | 41% | Mar 2005 | 14.9 | Yes | GB00B058DQ55 |

| 3T20 | 3.75 | 07 Sep 2020 | 24,320 | 1,161 | 4,993 | 18,166 | 75% | June 2010 | 10.2 | Yes | GB00B582JV65 |

| 1H21 | 1.50 | 22 Jan 2021 | 11,898 | 1 | 704 | 11,193 | 94% | Sep 2015 | 5.4 | no | GB00BYY5F581 |

| 3T21 | 3.75 | 07 Sep 2021 | 28,082 | 1,199 | 7,837 | 19,046 | 68% | Mar 2011 | 10.5 | Yes | GB00B4RMG977 |

| 4%22 | 4.00 | 07 Mar 2022 | 37,543 | 1,518 | 23,439 | 12,586 | 34% | Feb 2009 | 13.0 | Yes | GB00B3KJDQ49 |

| 3Q44 | 3.25 | 22 Jan 2044 | 27,052 | 362 | 2,785 | 23,905 | 88% | Oct 2012 | 31.2 | no | GB00B84Z9V04 |

| 3H45 | 3.50 | 22 Jan 2045 | 23,665 | 71 | 638 | 22,956 | 97% | June 2014 | 30.6 | no | GB00BN65R313 |

| 4Q49 | 4.25 | 07 Dec 2049 | 19,561 | 2,250 | 5,314 | 11,997 | 61% | Sep 2008 | 41.3 | Yes | GB00B39R3707 |

| 3T52 | 3.75 | 22 July 2052 | 21,965 | 587 | 6,753 | 14,625 | 67% | Sep 2011 | 40.8 | no | GB00B6RNH572 |

| 4Q55 | 4.25 | 07 Dec 2055 | 24,481 | 5,278 | 8,205 | 10,998 | 45% | May 2005 | 50.5 | Yes | GB00B06YGN05 |

| 4%60 | 4.00 | 22 Jan 2060 | 20,967 | 894 | 7,716 | 12,357 | 59% | Oct 2009 | 50.3 | no | GB00B54QLM75 |

| 2H65 | 2.50 | 22 July 2065 | 4,750 | Oct 2015 | 49.8 | no | GB00BYYMZX75 | ||||

| 3H68 | 3.50 | 22 July 2068 | 19,278 | 128 | 890 | 18,260 | 95% | June 2013 | 55.1 | no | GB00BBJNQY21 |

| Updates of £ quantities are infrequent and piecemeal. | |||||||||||

Julian D. A. Wiseman

Abstract: comment on gilt relative value, occasionally (meaning at least as many times as has been done).

Publication history: only at www.jdawiseman.com/papers/finmkts/gilt_relative_value.html. Usual disclaimer and copyright terms apply.

Contents:

• Introduction;

• 12th March 2016: 4Q55 still dear (indeed, 1bp dearer); 1H21 still cheap (but 2bp less cheap); and switch 2H65 → 3H68;

• 9th January 2016: 4Q55 still dear (indeed, ½bp dearer); 1H21 still cheap (but ½bp less cheap);

• 2nd January 2016: whole-curve gilt relative on one chart;

• 1st January 2016: 1H21 cheap to neighbours;

• 13th December 2015: ’44 and ’45 cheap; ’49 to ’60 still dear;

• 22nd November 2015: ’44 and ’45 cheap; ’49 to ’60 dear

• 22nd December 2017: links repaired.

There follows comment on gilt relative value. It is envisaged that further comment will be added occasionally, but this is not promised. Typically the comment requires a detailed chart, which is in the linked PDFs.

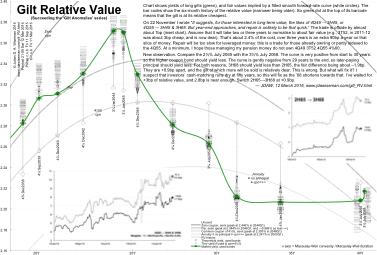

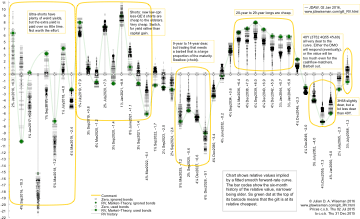

The chart (see detailed PDF) shows yields of long gilts (green), and fair values implied by a fitted smooth forward-rate curve (white circles). The bar codes show the six-month history of the relative value (narrower being older). So green dot at the top of its barcode means that the gilt is at its relative cheapest.

On 22 November I wrote “It suggests, for those interested in long-term value, the likes of 4Q49 → 3H45, or 4Q55 → 3H45 & 3H68. But year-end approaches, and repair is unlikely to be that quick.” The trade is offside by about 1bp (inset chart). Assume that it will take two or three years to normalise to about fair value (e.g., 3T52, in 2011-12 was about 3bp cheap, and is now dear). That’s about 2.4% of the cost, over three years is an extra 80bp a year on that slice of money. Repair will be too slow for leveraged money: this is a trade for those already owning or partly indexed to the 4Q55. At a minimum, I hope those managing my pension money do not own 4Q49 3T52 4Q55 4Q49.

New observation. Compare the 2½% July 2065 with the 3½% July 2068. The curve is very positive from start to 30 years: so the higher coupon bond should yield less. The curve is gently negative from 29 years to the end, so later-paying principal should yield less. For both reasons, 3H68 should yield less than 2H65, the fair difference being about –1.9bp. They are +0.9bp apart, and the gilt of which more will be sold is relatively dear. This is wrong. But what will fix it? I suspect that investors’ cash-matching runs dry at fifty years, so this will fix as the ’68 shortens towards that. I’ve waited for +3bp of relative value, and 2.8bp is near enough. Switch 2H65 → 3H68 at +0.9bp.

The next chart (see detailed PDF) shows yields and fair values of circa 5Y gilts.

On 01 Jan 2016, using data c.o.b. 31 Dec 2015, I wrote “the 1½% Jan 2021 gilt is cheap to neighbours. It could become less cheap, but even if not, it yields +10bp to the fair interpolation. The timing of the next auction is so obviously at the 5Y transition that demand might come ahead of it: before then switch into 1H21 from a mix of 3T20 (or 4T20) and 3T21 (or 4%22).”

It is now less cheap by about 2bp, which is pleasant enough. A short-term player hoping for a modest capital gain, presumably only attempted with lenient financing, should take the ten pence profit. Those investing non-leveraged cash should hold: the 1H21 is still cheap. From here the pace of capital gain is unlikely to be material; nonetheless, take the extra 8.6bp yield.

— JDAW, 12th March 2016, www.jdawiseman.com/gilt_RV.html

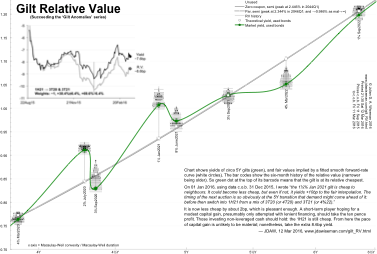

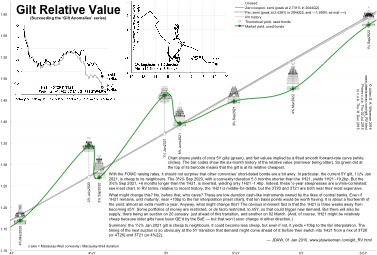

The chart (see detailed PDF) shows yields of long gilts (green), and fair values implied by a fitted smooth forward-rate curve (white circles). The bar codes show the six-month history of the relative value (narrower being older). So green dot at the top of its barcode means that the gilt is at its relative cheapest.

On 22 November I wrote “It suggests, for those interested in long-term value, the likes of 4Q49 → 3H45, or 4Q55 → 3H45 & 3H68. But year-end approaches, and repair is unlikely to be that quick.” The trade is offside by almost 0.5bp (inset chart). Rephrased more optimistically, entry is now half a basis point better. Assume that it will take two or three years to normalise to about fair value (e.g., 3T52, in 2011-12 was about 3bp cheap, and is now dear). On the 4Q55, 9.4bp is about 2.1% of the cost. Over three years is an extra 70bp a year on that slice of money. Repair will be too slow for leveraged money: this is a trade for those already owning or partly indexed to the 4Q55. At a minimum, I hope those managing my pension money do not own 4Q49 3T52 4Q55.

The next chart (see detailed PDF) shows yields and fair values of circa 5Y gilts.

On 01 Jan 2016, using data c.o.b. 31 Dec 2015, I wrote “the 1½% Jan 2021 gilt is cheap to neighbours. It could become less cheap, but even if not, it yields +10bp to the fair interpolation. The timing of the next auction is so obviously at the 5Y transition that demand might come ahead of it: before then switch into 1H21 from a mix of 3T20 (or 4T20) and 3T21 (or 4%22).”

A week later it is 0.5bp onside, which is indistinguishable from zero. The 1H21 is still cheap to neighbours: prefer; or prefer more.

— JDAW, 9th January 2016, www.jdawiseman.com/gilt_RV.html

Addendum, on a different subject. As a gilt analyst I collected data on gilts, some of which is still not widely available. So various spreadsheets and other scraps have been merged and published at www.jdawiseman.com/gilt_list.html. Its main use might be for those back-building yield curve models such as this: gilt first coupon amounts are not otherwise easily available. And most of the pre-1997 ISINs do not appear anywhere else on the web (e.g.).

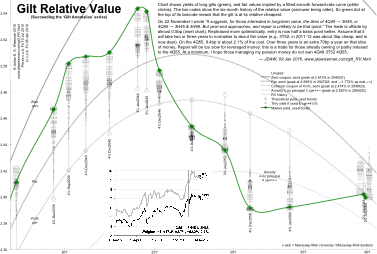

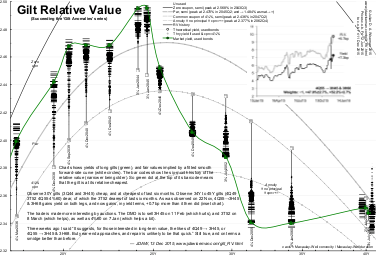

The chart (see detailed PDF) shows relative values implied by a fitted smooth forward-rate curve. The bar codes show the six-month history of the relative value, narrower being older. So green dot at the top of its barcode means that the gilt is at its relative cheapest.

Ultra-shorts have plenty of weird yields, but the extra yield is paid over so little time. Not worth the effort.

Shorts: new low-coupon less-QE’d shorts are cheap to the oldsters. Very cheap. Switch, for yield rather than capital gain.

9-year to 14-year gilts are dear, but trading that needs a barbell that is a large proportion of the maturity. Swallow (=hold).

20-year to 29-year longs are cheap.

40Y (3T52 4Q55 4%60) all very dear to the curve. Either the DMO will respond (eventually), or the value will be too much even for the cashflow-matchers. Barbell out.

3H68 slightly dear, but a lot less dear than 40Y.

— JDAW, 2nd January 2016, www.jdawiseman.com/gilt_RV.html

The chart (see detailed PDF) shows yields of circa 5Y gilts (green), and fair values implied by a fitted smooth forward-rate curve (white circles). The bar codes show the six-month history of the relative value (narrower being older). So green dot at the top of its barcode means that the gilt is at its relative cheapest.

With the FOMC raising rates, it should not surprise that other currencies’ short-dated bonds are a bit awry. In particular, the current 5Y gilt, 1½% Jan 2021, is cheap to its neighbours. The 3¾% Sep 2020, with a convexity÷duration 5.3 months shorter than the 1H21, yields 1H21 -19.2bp. But the 3¾% Sep 2021, +6 months longer than the 1H21, is inverted, yielding only 1H21 -1.4bp. Indeed, these ½-year steepnesses are un/mis-correlated: see inset chart. In RV terms, relative to recent history, the 1H21 is middle-for-diddle, but the 3T20 and 3T21 are both near their most expensive.

What might change this? No, before that, who cares? These are low-duration cash-like instruments owned by the likes of central banks. Even if 1H21 remains, until maturity, near +10bp to the fair interpolation (inset chart), that ten basis points would be worth having. It is about a fourteenth of the yield: almost an extra month a year. Anyway, what might change this? The obvious imminent fact is that the 1H21 is three weeks away from becoming ≤5Y. Some portfolios of money are restricted, or de facto restricted, to ≤5Y, so that could trigger new demand. But there will also be supply, there being an auction on 20 January just ahead of this transition, and another on 02 March. (And, of course, 1H21 might be relatively cheap because older gilts have been QE’d by the BoE — but that won’t soon change in either direction.)

Summary: the 1½% Jan 2021 gilt is cheap to neighbours. It could become less cheap, but even if not, it yields +10bp to the fair interpolation. The timing of the next auction is so obviously at the 5Y transition that demand might come ahead of it: before then switch into 1H21 from a mix of 3T20 (or 4T20) and 3T21 (or 4%22).

— JDAW, 1st January 2016, www.jdawiseman.com/gilt_RV.html

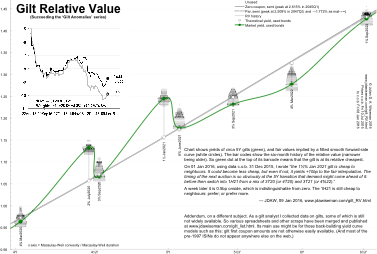

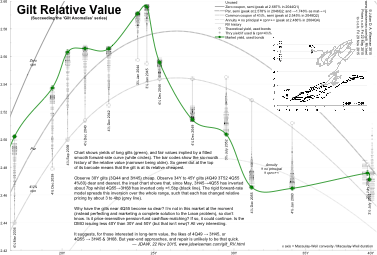

The chart (see detailed PDF) shows yields of long gilts (green), and fair values implied by a fitted smooth forward-rate curve (white circles). The bar codes show the six-month history of the relative value (narrower being older). So a green dot at the top of its barcode means that the gilt is at its relative cheapest.

Observe 30Y gilts (3Q44 and 3H45) cheap, and at cheapest of last six months. Observe 34Y to 45Y gilts (4Q49 3T52 4Q55 4%60) dear, of which the 3T52 dearest of last six months. As was observed on 22 Nov, 4Q55 → 3H45 & 3H68 gains yield on both legs, and now gains, in yield terms, +0.7bp more than it then did (inset chart).

The trade is made more interesting by auctions. The DMO is to sell 3H45 on 11 Feb (which hurts), and 3T52 on 8 March (which helps), as well as 4%60 on 7 Jan (which helps a bit). Three weeks ago I said “It suggests, for those interested in long-term value, the likes of 4Q49 → 3H45, or 4Q55 → 3H45 & 3H68. But year-end approaches, and repair is unlikely to be that quick.” Still true, and on terms a smidge better than before.

— JDAW, 13th December 2015, www.jdawiseman.com/gilt_RV.html

The chart (see detailed PDF) shows yields of long gilts (green), and fair values implied by a fitted smooth forward-rate curve (white circles). The bar codes show the six-month history of the relative value (narrower being older). So a green dot at the top of its barcode means that the gilt is at its relative cheapest.

Observe that 30Y gilts (the 3Q44 and 3H45) are cheap. Observe that 34Y to 45Y gilts (4Q49 3T52 4Q55 4%60) are dear and dearest. The inset chart shows that, since May, 3H45→4Q55 has inverted about 7bp whilst 4Q55→3H68 has inverted only ≈1.5bp (black line). The rigid forward-rate model spreads this inversion over the whole range, such that each has changed relative pricing by about 3 to 4bp (grey line).

Why have the gilts near 4Q55 become so dear? I’m not in this market at the moment (instead perfecting and marketing a complete solution to the Lɪʙᴏʀ problem), so don’t know. Is it price-insensitive pension-fund cashflow-matching? If so, it could continue. Is the DMO issuing less 40Y than 30Y and 50Y (but that isn’t new)? All very interesting.

It suggests, for those interested in long-term value, the likes of 4Q49 → 3H45, or 4Q55 → 3H45 & 3H68. But year-end approaches, and repair is unlikely to be that quick.

— JDAW, 22nd November 2015, www.jdawiseman.com/gilt_RV.html

In December 2017 the DMO rotted all incoming links. Links in the above have been replaced. Other content is unchanged.

| Main index | Top | About author |