![]()

![]()

| Main index | Financial Markets index | About author |

![]()

![]()

Julian D. A. Wiseman

Abstract: static details of non-conventional gilts: index-linked with 3-month and 8-month lags; ‘perpetuals’; floating-rate; and variable-rate.

Publication history: only at www.jdawiseman.com/papers/finmkts/papers/gilt_statics_non-conventionals.html. Usual disclaimer and copyright terms apply.

Contents: • Introduction; • Canadian-style Index-Linked Gilts, with three-month lag; • Old-style Index-Linked Gilts, with eight-month lag; • The ‘Perpetuals’; • Floating-Rate Gilts; • Variable-Rate Gilts.

Also see details about conventional gilts.

As a gilt analyst I collected data on gilts, some of which is still not widely available, so is being published here. Much of the gathered data is about conventionals, which can be found at www.jdawiseman.com/papers/finmkts/gilt_statics.html. This page holds data relating to the index-linked gilts (both three-month and eight-month), perpetuals, floating-rate gilts, and variable-rate gilts.

Most of the fields/columns have the same meaning as those in www.jdawiseman.com/papers/finmkts/gilt_statics.html, wherein descriptions can be found.

In Sep 2001 the DMO consulted “on whether to adopt a new design for new issues of index-linked gilts”. JDAW’s reply advised against; and in January 2002 the DMO concurred. Then in Dec 2004 the DMO consulted about ultra-long gilts (JDAW’s reply), announcing (not consulting) that:

The DMO is also taking the opportunity to introduce a new indexation structure into any new index-linked gilts issued from 2005-06. Specifically, any new index-linked gilt issued from 2005-06 will use a three as opposed to the current eight-month indexation lag to the RPI. This reflects the adoption of a three-month lag as current international best practice. … Note that the DMO does not intend to introduce a deflation floor. The introduction of any new three-month lag index-linked gilts from 2005-06 does not mean that current eight-month lag index-linked gilts cannot be re-opened.

It happens that, in January 2004 the LSE switched from numeric Sᴇᴅᴏʟs to alphanumeric Sᴇᴅᴏʟs. So, for all ILGs with an eight-month lag, characters 3–12 of the ISIN are numeric; for all ILGs with a three-month lag character 5 of the ISIN is ‘B’.

A comment on coupons not being zero: the many small payments entail some small administration cost. But those same payments allow tracing of missing holders. If a natural owner dies, or a corporate owner is wound up, with a zero coupon bond this might not be discovered until an attempt is made to pay the principal, perhaps decades later. With a positive coupon the failed payment would be discovered within half a year, soon enough for there to be a good chance of finding the successor owner. This seems sensible. But observe that zero-coupon conventionals are issued by Germany (0% 15 Aug 2050), Switzerland (0% 24 July 2039), and others. Further this argument would obviously fail for long-dated strips.

Coupon: the coupons of index-linked gilts, both 3- and 8-monthers, are integer multiples of ⅛%. Even large coupons have been rounded to 12½ basis points: e.g., 4⅛% 30s, 4⅜% 04s, 4⅝% 98s, as well as 1⅞% 22s. Coupons have always been strictly positive, so ≥ 0⅛%, even with very negative real yields.

First coupon amount: real first coupon amounts are not rounded, and are shown in a format that can be copy-pasted into Excel. Cash first coupon amounts are rounded “to six places of decimals”.

Both 3- abnd 8-month linkers have Bloomberg ticker UKTI.

| Short Name |

Cpn | Maturity | Base index | First settle date |

First coupon date |

First coupon, real | Orig. term |

Formal name | ISIN, FIGI |

Notes |

|---|---|---|---|---|---|---|---|---|---|---|

| 73s | 0.125 | 22 Mar 2073 | 308.32 | 24 Nov 2021 | 22 Mar 2022 | =(0.125/2)*(118/181) | 51.32 | 0⅛% Index-linked Treasury Gilt 2073 | GB00BM8Z2W66 BBG013FHV1K9 |

|

| 68s | 0.125 | 22 Mar 2068 | 249.7 | 25 Sep 2013 | 22 Mar 2014 | =(0.125/2)*(178/181) | 54.49 | 0⅛% Index-linked Treasury Gilt 2068 | GB00BDX8CX86 BBG0057VMB12 |

68s was longest linker from issue until Nov 2021 when 73s was issued, the previous longest having been 62s. 68s, on 09 Oct 2013, had a modified duration of 52.78 years, perhaps a record for a gov’t bond. |

| 65s | 0.125 | 22 Nov 2065 | 260.43448 | 24 Feb 2016 | 22 May 2016 | =(0.125/2)*(88/182) | 49.74 | 0⅛% Index-linked Treasury Gilt 2065 | GB00BD9MZZ71 BBG00C63FZY9 |

|

| 62s | 0.375 | 22 Mar 2062 | 235.82903 | 26 Oct 2011 | 22 Mar 2012 | =(0.375/2)*(148/182) | 50.41 | 0⅜% Index-linked Treasury Gilt 2062 | GB00B4PTCY75 BBG0025LSRV9 |

62s was longest linker from issue until Sep 2013 when 68s was issued, the previous longest having been 55s. |

| 58s | 0.125 | 22 Mar 2058 | 255.8871 | 30 July 2014 | 22 Mar 2015 | =(0.125/2)*(1+54/184) | 43.64 | 0⅛% Index-linked Treasury Gilt 2058 | GB00BP9DLZ64 BBG006T1F9W1 |

58s, syndication result on 29 July 2014: “a negative real yield for the first time in a DMO index-linked gilt syndication.” |

| 56s | 0.125 | 22 Nov 2056 | 264.88333 | 30 Nov 2016 | 22 May 2017 | =(0.125/2)*(173/181) | 39.98 | 0⅛% Index-linked Treasury Gilt 2056 | GB00BYVP4K94 BBG00FBHPV82 |

|

| 55s | 1.250 | 22 Nov 2055 | 192.2 | 23 Sep 2005 | 22 May 2006 | =(1.25/2)*(1+60/184) | 50.16 | 1¼% Index-linked Treasury Gilt 2055 | GB00B0CNHZ09 BBG0000BHW05 |

55s is the first-issued of the Canadian-style UK ‘linkers’ and hence first of the ILGs paying 22May/Nov (pre-announcement, announcement); the first named Index-linked Treasury Gilt rather than Index-linked Treasury Stock; and the first linker with a non-numeric Sᴇᴅᴏʟ (not counting the temporary Sᴇᴅᴏʟs of reopenings). 55s was longest linker from issue until Oct 2011 when 62s was issued, the previous longest having been the 8-monther 35s. |

| 54s | 1.250 | 22 Nov 2054 | 378.58065 | 13 Mar 2024 | 22 May 2024 | =(1.25/2)*(70/182) | 30.69 | 1¼% Index-linked Treasury Gilt 2054 | GB00BPSNBG80 BBG01LQG9623 |

|

| 52s | 0.250 | 22 Mar 2052 | 242.05 | 26 Sep 2012 | 22 Mar 2013 | =(0.25/2)*(177/181) | 39.49 | 0¼% Index-linked Treasury Gilt 2052 | GB00B73ZYW09 BBG003DDJJ99 |

|

| 51s | 0.125 | 22 Mar 2051 | 294.11071 | 10 Feb 2021 | 22 Sep 2021 | =(0.125/2)*(1+40/181) | 30.11 | 0⅛% Index-linked Treasury Gilt 2051 | GB00BNNGP882 BBG00Z0Y5WF5 |

|

| 50s | 0.500 | 22 Mar 2050 | 213.4 | 25 Sep 2009 | 22 Mar 2010 | =(0.5/2)*(178/181) | 40.49 | 0½% Index-linked Treasury Gilt 2050 | GB00B421JZ66 BBG0000NBYJ1 |

The first to be issued of the ILGs paying 22Mar/Sep (announcement). |

| 49s | 1.875 | 22 Sep 2049 | 391.95806 | 12 Mar 2025 | 22 Sep 2025 | =(1.875/2)*(1+10/181) | 24.53 | 1⅞% Index-linked Treasury Gilt 2049 | GB00BT7J0134 BBG01SCVGS97 |

|

| 48s | 0.125 | 10 Aug 2048 | 274.79333 | 08 Nov 2017 | 10 Feb 2018 | =(0.125/2)*(94/184) | 30.76 | 0⅛% Index-linked Treasury Gilt 2048 | GB00BZ13DV40 BBG00J2D03W5 |

The first to be issued of the ILGs paying 10Feb/Aug (announcement). |

| 47s | 0.750 | 22 Nov 2047 | 207.76667 | 21 Nov 2007 | 22 May 2008 | =(0.75/2)*(1+1/184) | 40.00 | 0¾% Index-linked Treasury Gilt 2047 | GB00B24FFM16 BBG0000L4515 |

|

| 46s | 0.125 | 22 Mar 2046 | 257.79 | 24 June 2015 | 22 Sep 2015 | =(0.125/2)*(90/184) | 30.74 | 0⅛% Index-linked Treasury Gilt 2046 | GB00BYMWG366 BBG009CQDGT8 |

|

| 45s | 0.625 | 22 Mar 2045 | 363.94 | 27 Apr 2023 | 22 Sep 2023 | =(0.625/2)*(148/184) | 21.90 | 0⅝% Index-linked Treasury Gilt 2045 | GB00BMF9LH90 BBG01G6SV4F6 |

|

| 44s | 0.125 | 22 Mar 2044 | 242.42258 | 25 July 2012 | 22 Mar 2013 | =(0.125/2)*(1+59/184) | 31.66 | 0⅛% Index-linked Treasury Gilt 2044 | GB00B7RN0G65 BBG0036PB7W8 |

|

| 42s | 0.625 | 22 Nov 2042 | 212.46452 | 24 July 2009 | 22 Nov 2009 | =(0.625/2)*(121/184) | 33.33 | 0⅝% Index-linked Treasury Gilt 2042 | GB00B3MYD345 BBG0000G0PJ7 |

|

| 41s | 0.125 | 10 Aug 2041 | 280.05484 | 12 July 2018 | 10 Feb 2019 | =(0.125/2)*(1+29/181) | 23.08 | 0⅛% Index-linked Treasury Gilt 2041 | GB00BGDYHF49 BBG00L991NQ4 |

|

| 40s | 0.625 | 22 Mar 2040 | 216.52258 | 28 Jan 2010 | 22 Sep 2010 | =(0.625/2)*(1+53/181) | 30.15 | 0⅝% Index-linked Treasury Gilt 2040 | GB00B3LZBF68 BBG0000GW3R2 |

|

| 39s | 0.125 | 22 Mar 2039 | 296.72581 | 26 May 2021 | 22 Sep 2021 | =(0.125/2)*(119/184) | 17.82 | 0⅛% Index-linked Treasury Gilt 2039 | GB00BLH38265 BBG010WR4WB6 |

|

| 38s | 1.750 | 22 Sep 2038 | 397.6 | 11 June 2025 | 22 Sep 2025 | =(1.75/2)*(103/184) | 13.28 | 1¾% Index-linked Treasury Gilt 2038 | GB00BMY62Z61 BBG01V8NPFG3 |

|

| 37s | 1.125 | 22 Nov 2037 | 202.24286 | 21 Feb 2007 | 22 May 2007 | =(1.125/2)*(90/181) | 30.75 | 1⅛% Index-linked Treasury Gilt 2037 | GB00B1L6W962 BBG0000GRYH1 |

|

| 36s | 0.125 | 22 Nov 2036 | 260.01935 | 11 Mar 2016 | 22 May 2016 | =(0.125/2)*(72/182) | 20.70 | 0⅛% Index-linked Treasury Gilt 2036 | GB00BYZW3J87 BBG00CCP0450 |

|

| 35s | 1.125 | 22 Sep 2035 | 390.88065 | 29 Jan 2025 | 22 Sep 2025 | =(1.125/2)*(1 + 52/181) | 10.65 | 1⅛ Index-linked Treasury Gilt 2035 | GB00BT7HZZ68 BBG01RXGT318 |

|

| 34s | 0.750 | 22 Mar 2034 | 232.22903 | 25 May 2011 | 22 Sep 2011 | =(0.75/2)*(120/184) | 22.83 | 0¾% Index-linked Treasury Gilt 2034 | GB00B46CGH68 BBG001PNKYF6 |

|

| 33s | 0.750 | 22 Nov 2033 | 372.24 | 28 June 2023 | 22 Nov 2023 | =(0.75/2)*(147/184) | 10.40 | 0¾% Index-linked Treasury Gilt 2033 | GB00BMF9LJ15 BBG01H3VNM32 |

|

| 32s | 1.250 | 22 Nov 2032 | 217.13226 | 29 Oct 2008 | 22 May 2009 | =(1.25/2)*(1+24/184) | 24.06 | 1¼% Index-linked Treasury Gilt 2032 | GB00B3D4VD98 BBG0000VN0M0 |

|

| 31s | 0.125 | 10 Aug 2031 | 293.60323 | 28 Jan 2021 | 10 Aug 2021 | =(0.125/2)*(1+13/184) | 10.53 | 0⅛% Index-linked Treasury Gilt 2031 | GB00BNNGP551 BBG00YZD3PJ9 |

|

| 29s | 0.125 | 22 Mar 2029 | 237.42 | 23 Nov 2011 | 22 Mar 2012 | =(0.125/2)*(120/182) | 17.33 | 0⅛% Index-linked Treasury Gilt 2029 | GB00B3Y1JG82 BBG002802G17 |

|

| 28s | 0.125 | 10 Aug 2028 | 279.23333 | 21 June 2018 | 10 Feb 2019 | =(0.125/2)*(1+50/181) | 10.14 | 0⅛% Index-linked Treasury Gilt 2028 | GB00BZ1NTB69 BBG00L4P50W2 |

|

| 27s | 1.250 | 22 Nov 2027 | 194.06667 | 26 Apr 2006 | 22 Nov 2006 | =(1.25/2)*(1+26/181) | 21.57 | 1¼% Index-linked Treasury Gilt 2027 | GB00B128DH60 BBG0000C61W8 |

|

| 26s | 0.125 | 22 Mar 2026 | 258.24194 | 16 July 2015 | 22 Sep 2015 | =(0.125/2)*(68/184) | 10.68 | 0⅛% Index-linked Treasury Gilt 2026 | GB00BYY5F144 BBG009KCJHC0 |

|

| New 24s | 0.125 | 22 Mar 2024 | 242.41935 | 12 Oct 2012 | 22 Mar 2013 | =(0.125/2)*(161/181) | 11.44 | 0⅛% Index-linked Treasury Gilt 2024 | GB00B85SFQ54 BBG003G3FFD5 |

New 24s, on 11 April 2013 was the first gilt to be auctioned at a real yield below negative one percent, indeed at −1.262%. Principal payment at maturity = £156.061000 per £100. |

| 22s | 1.875 | 22 Nov 2022 | 205.65806 | 11 July 2007 | 22 Nov 2007 | =(1.875/2)*(134/184) | 15.36 | 1⅞% Index-linked Treasury Gilt 2022 | GB00B1Z5HQ14 BBG0000CDS24 |

22s, on 23 Aug 2011, was the first gilt to be auctioned at a negative yield (albeit a negative real yield). Principal payment at maturity = £168.668000 per £100. |

| 19s | 0.125 | 22 Nov 2019 | 249.80645 | 21 Aug 2013 | 22 Nov 2013 | =(0.125/2)*(93/184) | 6.25 | 0⅛% Index-linked Treasury Gilt 2019 | GB00BBDR7T29 BBG0053D1Q98 |

Principal payment at maturity = £116.574000 per £100. |

| 17s | 1.250 | 22 Nov 2017 | 193.725 | 08 Feb 2006 | 22 May 2006 | =(1.25/2)*(103/181) | 11.79 | 1¼% Index-linked Treasury Gilt 2017 | GB00B0V3WQ75 BBG0000BPHW4 |

Principal payment at maturity = £141.943000 per £100 (the first principal amount for which the DMO was the calculation agent). |

The introduction of inflation-linked securities was announced in the Budget Speech on 10 March 1981. Further explanation was published in May 1981. This was to be the first large inflation-linked government debt market.

These old-style ILGs have payments with an eight-month lag: the nominal÷real factor is the RPI eight months before the month of payment divided by the RPI eight months before the month of first issue. The eight-month lag ensures that the £ value of a coupon is known before the start of that coupon period, which can then be used for the calculation of accrued interest. However, in January 1987 the RPI was re-based from 394.5 to 100, so some base indices are re-based with a “/3.945”. Prices are quoted nominal.

Nominal payments are rounded: initially to the nearest penny per £100; for ILGs issued after Feb 1982 (so starting with 88s) the number of decimal places was upped to 4; and for the 35s only to 6 decimal places. This is in the “D.P.” column.

For 8-month ILGs issued ≤1992, so for those up to 30s, a change “to the coverage or the basic calculation of the Index … which would be materially detrimental to stockholders” would give holders a right to put the gilt back to HMT at inflation-adjusted par. But for 35s, and similarly for the 3-monthers, the index could be replaced with another index that “continues the function of measuring changes in the level of UK retail prices”.

| Short Name |

Cpn | Maturity | Base index | D.P. | First settle date |

First coupon date |

First cpn amount |

Orig. term |

Formal name | ISIN, FIGI |

Notes |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 35s | 2.000 | 26 Jan 2035 | 173.6 | 6 | 10 July 2002 | 26 Jan 2003 | 1.099091 | 32.54 | 2% Index-Linked Treasury Stock 2035 | GB0031790826 BBG0000423Y4 |

35s was the last-issued of the UK ‘linkers’ with an eight-month lag; the last to be named Index-linked Treasury Stock rather than Index-linked Treasury Gilt; and the last with a numeric Sᴇᴅᴏʟ. It is the only eight-month linker for which payments are rounded to six decimal places; the only for which the calculation agent is the DMO rather than the BoE; and the only of which the first coupon was computed with the post-1998 Act/Act formula. 35s was also the only 8-monther for which the index could be replaced with another index that “continues the function of measuring changes in the level of UK retail prices”, without giving holders a right to put the gilt back to HMT at inflation-adjusted par. Unusual details: Methodology for calculating the first dividend payment and the accrued interest for 2% Index-linked Treasury Stock 2035. The auction of 35s on 25 Sep 2002 was uncovered: £900m for sale; £853.12m bids received; 0.95× covered: “The unallocated part of the amount on offer at this auction is being held in official portfolios.” Needless danger: there is a solution. |

| 30s | 4.125 | 22 July 2030 | 135.1 | 4 | 16 June 1992 | 22 Jan 1993 | 2.6102 | 38.10 | 4⅛% Index-Linked Treasury Stock 2030 | GB0008932666 BBG00001FPJ4 |

Of the gilts of which the first coupon was computed with the old Act/365 formula, 30s will be the last to mature (preceded by 6%28). The auction of 30s on 28 Apr 1999 was uncovered: £500m for sale; £470.3m bids received; 0.94× covered: “The unallotted part of the amount on offer at the auction is being held in official portfolios. It will not be made available to the market at a price below the striking price for a period of at least two-months.” Needless danger: there is a solution. |

| Old 24s | 2.500 | 17 July 2024 | =385.3/3.945 | 4 | 31 Dec 1986 | 17 July 1987 | 1.1809 | 37.55 | 2½% Index-Linked Treasury Stock 2024 | GB0008983024 BBG00000KDS7 |

Principal payment at maturity = £386.3089 per £100 ≈ 100 × 377.3 × 3.945/385.3 ≈ 386.30898, which was then, per ¶12 of the prospectus, “… to four places of decimals rounded to the nearest figure below”. |

| 20s | 2.500 | 16 Apr 2020 | =327.3/3.945 | 4 | 12 Oct 1983 | 16 Apr 1984 | 1.1138 | 36.51 | 2½% Index-Linked Treasury Stock 2020 | GB0009081828 BBG00000KDR8 |

Of the gilts issued before 29 May 1985, linker 20s was the last to mature (preceded by 16s). Principal payment at maturity = £351.5907 per £100 ≈ 100 × 291.7 × 3.945/327.3. |

| 16s | 2.500 | 26 July 2016 | =322/3.945 | 4 | 19 Jan 1983 | 26 July 1983 | 1.0911 | 33.52 | 2½% Index-Linked Treasury Stock 2016 | GB0009075325 BBG00000KDQ9 |

Of the gilts issued before 29 May 1985, linker 16s was the second-last to mature (followed by 20s). Principal payment at maturity = £318.2953 per £100. |

| 13s | 2.500 | 16 Aug 2013 | =351.9/3.945 | 4 | 21 Feb 1985 | 16 Aug 1985 | 1.228 | 28.49 | 2½% Index-Linked Treasury Stock 2013 | GB0009036715 BBG00000KDP0 |

Principal payment at maturity = £276.6768 per £100. |

| 11s | 2.500 | 23 Aug 2011 | =294.1/3.945 | 2 | 28 Jan 1982 | 23 Aug 1982 | 1.26 | 29.57 | 2½% Index-Linked Treasury Stock 2011 | GB0009063578 BBG00000KDN2 |

Principal payment at maturity = £306.37 per £100. |

| 09s | 2.500 | 20 May 2009 | =310.7/3.945 | 4 | 19 Oct 1982 | 20 May 1983 | 1.5161 | 26.59 | 2½% Index-Linked Treasury Stock 2009 | GB0009071563 BBG00081MWT2 |

Principal payment at maturity = £277.3054 per £100. |

| 06s | 2.000 | 19 July 2006 | =274.1/3.945 | 2 | 08 July 1981 | 19 Jan 1982 | 0.92 | 25.03 | 2% Index-Linked Treasury Stock 2006 | GB0009061317 BBG00072MKQ0 |

On 19 July 2001 £½bn 06s switch-auctioned into 16s: announcement; memorandum; result. Principal payment at maturity = £278.63 per £100. |

| 04s | 4.375 | 21 Oct 2004 | 135.6 | 4 | 23 Sep 1992 | 21 Apr 1993 | 1.8017 | 12.08 | 4⅜% Index-Linked Treasury Stock 2004 | GB0009982686 BBG0006J7R22 |

It used to be that re-openings of gilts did not have a “Re-opening Prospectus”. The first to do so was 04s, in Aug 1998. Principal payment at maturity = £135.5457 per £100. |

| 03s | 2.500 | 20 May 2003 | =310.7/3.945 | 4 | 27 Oct 1982 | 20 May 1983 | 1.4592 | 20.56 | 2½% Index-Linked Treasury Stock 2003 | GB0009066365 BBG00066HZH5 |

Principal payment at maturity = £225.5011 per £100. |

| 01s | 2.500 | 24 Sep 2001 | =308.8/3.945 | 4 | 26 Aug 1982 | 24 Mar 1983 | 19.08 | 2½% Index-Linked Treasury Stock 2001 | GB0009065391 BBG000K2LKC1 |

Principal payment at maturity = £218.5846 per £100. | |

| 99s | 2.500 | 22 Nov 1999 | =322.9/3.945 | 4 | 04 May 1983 | 22 Nov 1983 | 1.206 | 16.55 | 2½% Index-Linked Treasury Convertible Stock 1999 |

GB0009074575 BBG0004T89N8 |

Nickname = “Maggie Mays”, because convertible into 10Q99. And almost all converted, because Maggie did. Principal payment at maturity = £200.4876 per £100 (the BoE press release containing a titling error). |

| 98s | 4.625 | 27 Apr 1998 | 135.6 | 4 | 21 Sep 1992 | 27 Apr 1993 | 2.2448 | 5.60 | 4⅝% Index-Linked Treasury Stock 1998 | GB0009982579 BBG0003K0P32 |

Principal payment at maturity = £116.8879 per £100. |

| 96s | 2.000 | 16 Sep 1996 | =267.9/3.945 | 2 | 27 Mar 1981 | 16 Sep 1981 | 0.8 | 15.47 | 2% Index-Linked Treasury Stock 1996 | GB0009056556 BBG00039CGB5 |

The first-issued UK ‘linker’. And the joys of inefficient markets! According to the BoE Quarterly Bulletin, June 1981, p176, bidding was in multiples of 25 pence (≈ 1.88bp), and prices bid ranged from ≤£89¾ (real yield≈2.76%) to ≥£130 (≈−0.3bp). It was issued at par, suggesting that the BoE also didn’t know the right price. Which suggests that this auction should have been a syndication (in the author’s opinion, the only post-WW2 sale which should have been a syndication). Re bidding resolution, I have argued that it now should be “at least as fine as 0.1¢ or an eighth of a thirty-second”. Principal payment at maturity = £221.17 per £100. |

| 94s | 2.000 | 16 May 1994 | 102.9 | 4 | 02 June 1988 | 5.96 | 2% Index-Linked Treasury Stock 1994 | GB0009079632 |

Principal payment at maturity = £137.9008 per £100. | ||

| 92s | 2.000 | 23 Mar 1992 | =385.8/3.945 | 4 | 18 Feb 1987 | 23 Sep 1987 | 5.10 | 2% Index-Linked Treasury Stock 1992 | GB0009077925 |

Principal payment at maturity = £136.8172 per £100. | |

| 90s | 2.000 | 25 Jan 1990 | =333.9/3.945 | 4 | 05 Jan 1984 | 25 July 1984 | 1.1333 | 6.06 | 2% Index-Linked Treasury Stock 1990 | GB0009095943 |

A prospectus dated 29 Dec 1983 was published in The Times of 02 Jan 1984. Principal payment at maturity = £135.8715 per £100. |

| 88s | 2.000 | 30 Mar 1988 | =297.1/3.945 | 4 | 19 Mar 1982 | 30 Sep 1982 | 0.9996 | 6.03 | 2% Index-Linked Treasury Stock 1988 | GB0009062166 |

A prospectus dated 09 Mar 1982 was published in The Times of 11 Mar 1982. Principal payment at maturity = £135.1736 per £100. |

Wikipedia says that “Sukuk are "securities of equal denomination representing individual ownership interests in a portfolio of eligible existing or future assets."”. The UK’s process started in Nov 2007 with a consultation, Government sterling sukuk issuance, the June 2008 response saying:

The Government’s objectives for Islamic finance are to:

entrench London as a leading centre for Islamic finance in the world; and

to ensure that all British citizens can participate in the financial system regardless of faith.

There was then a long gap, with an occasional comment such as that in Jan 2011: ‘The Government had reviewed the case for the issuance of sovereign sukuk. The Government had decided not to issue sovereign sukuk because it was judged not to provide value for money for the Exchequer but it would keep the situation under review.” Finally, the first was issued in 2014, the second in 2021. They have Bloomberg ticker UKSUK.

UK sukuk “use the commonly used Al-Ijara structure”, which is explained on IslamicMarkets.com.

| Maturity | Profit rate |

First settle date |

First Dist’n date |

Orig. term |

ISIN, FIGI |

Notes |

|---|---|---|---|---|---|---|

| 22 July 2026 | 0.333 | 01 Apr 2021 | 22 July 2021 | 5.31 | XS2317288996 BBG00ZS048H1 |

Planning for this had started in late 2019 (invitation to tender, 26 Sep 2019; appointment of legal advisors, 11 Nov 2019), but was likely delayed by COVID. HMT press notice of 25 Mar 2021: UK bolsters Islamic finance offering with second Sukuk. |

| 22 July 2019 | 2.036 | 02 July 2014 | 22 Jan 2015 | 5.05 | XS1079249816 BBG006N6MBX2 |

No obvious press statement on issue. A few weeks before, on 12 June 2014, there had been Britain set to become first western nation to issue a sovereign Islamic bond. Shortly after the transaction it was mentioned in the FT: UK sukuk bond sale attracts £2bn in orders. |

Much funding used to be via callable gilt-edged securities with no final maturity date. Income, and more income, and no promise of ever seeing the principal. Some could be redeemed only by Parliament, which delegated this power to the DMO in the Finance Act 2015, s.124 (see announcement in §A.1 on p93 of the Autumn Statement 2014, and explanatory notes for the legislation). All the perpetuals were redeemed during 2015. The following table draws heavily on (and adds to) pp23–24 of the DMO Annual Review 2014–15.

| Formal name | Amount in issue at redemption |

Dividend dates |

First settle date |

First call date |

Redeemed (announced) |

ISIN, FIGI |

Notes |

|---|---|---|---|---|---|---|---|

| 4% Consolidated Loan (1957 or after) | £218.4m | 1 Feb/Aug | 19 Jan 1927 | 01 Feb 1957 | 1 Feb 2015 (31 Oct 2014) |

GB0002163466 BBG00000KF66 |

Issued for cash and in exchange for 5% Treasury Bonds 1927, 4% National War Bonds 1927, 5% National War Bonds 1927, 5% Treasury Bonds 1933–1935, 4½% Treasury Bonds 1932–1934 and 4½% Treasury Bonds 1930–1932. |

| 3½% War Loan (1952 or after) | £1938.6m | 1 Jun/Dec | 01 Dec 1932 | 01 Dec 1952 | 9 Mar 2015 (03 Dec 2014: HMT, DMO) |

GB0009386284 BBG00000KF57 |

Issued in exchange for 5% War Loan 1929–1947 (wherein are links to discussion). See the London Gazettes of 30 June 1932 and 12 July 1932, and the Edinburgh Gazette of 05 July 1932. The National Debt Act 1972, s.13, is entitled “Provision as to 3½% War Loan”, and says “The principal of and interest on 3½% War Loan, and any expenses incurred in connection with the redemption thereof, shall be charged on the National Loans Fund with recourse to the Consolidated Fund.” Presumably it had previously been a charge on a different account: explanation welcomed. The shortest Bloomberg ticker for 3½% War Loan was ZZ2036940 Govt. Also see Jeremy Wormell’s letter to the Financial Times published 19 Mar 2012. |

| 3½% Conversion Loan (1961 or after) | £15.6m | 1 Apr/Oct | 01 Apr 1921 | 01 Apr 1961 | 1 Apr 2015 (17 Dec 2014) |

GB0002212099 BBG00000KF48 |

Issued in exchange for 5% National War Bonds 1922, 1923 (Apr and Sep), 1924 (Feb and Oct),1925 (Apr and Sept). Had an active sinking fund. The shortest Bloomberg ticker for 3½% Conversion was ZZ2036932 Govt. |

| 3% Treasury Stock (1966 or after) | £34.6m | 1 Apr/Oct | 01 Mar 1946 | 05 Apr 1966 | 8 May 2015 (06 Feb 2015: HMT, DMO) |

GB0009031211 BBG00000KF20 |

Issued in exchange for Bank Stock in accordance with the provisions of the Bank of England Act 1946. |

| 2¾% Annuities | £0.7m | 5 Jan/Apr/Jul/Oct | 17 Oct 1884 | 05 Jan 1905 | 5 July 2015 (27 Mar 2015) |

GB0000436294 BBG000022GR7 |

Issued by exchange for New 3% Annuities, Reduced 3% Annuities and Consolidated 3% Annuities, as detailed in the The London Gazette, 8 Aug 1884, pp3573-4. |

| 2½% Treasury Stock (1975 or after) | £220.9m | 1 Apr/Oct | 28 Oct 1946 | 01 Apr 1975 | 5 July 2015 (27 Mar 2015) |

GB0009031096 BBG00000KDV3 |

Issued for cash. The shortest Bloomberg ticker for 2½% Treasury was ZZ2036973 Govt. |

| 2½% Consolidated Stock (1923 or after) | £162.1m | 5 Jan/Apr/Jul/Oct | 5 Apr 1888 | 05 Apr 1923 | 5 July 2015 (27 Mar 2015) |

GB0002163805 BBG00000KDT6 |

Issued in exchange for Consolidated 3% Annuities (1752), Reduced 3% Annuities (1752) and New 3% Annuities (1855). The shortest Bloomberg ticker for 2½% Consols was ZZ2036965 Govt. |

| 2½% Annuities | £0.9m | 5 Jan/Apr/Jul/Oct | 13 Jun 1853 | 05 Jan 1905 | 5 July 2015 (27 Mar 2015) |

GB0000436070 BBG000022GQ8 |

Issued in exchange for South Sea Stock, Old South Sea 3% Annuities, New South Sea 3% Annuities, Bank 3% Annuities (1726) and 3% Annuities (1751). The shortest Bloomberg ticker for 2½% Annuities was GG7183682 Govt. |

In 1994, with a bond-market crash continuing, the BoE issued a floater, paying (a private fixing of) Libid minus 12½bp. Two years later a second was issued.

There was a daily market fixing of Lɪʙᴏʀ, but not of Libid. Why use a private fixing? Was the BoE already aware of the problems that would later become the Lɪʙᴏʀ scandal? Or was it beneath the Old Lady’s dignity to use the same fixing as everybody else? Or both?

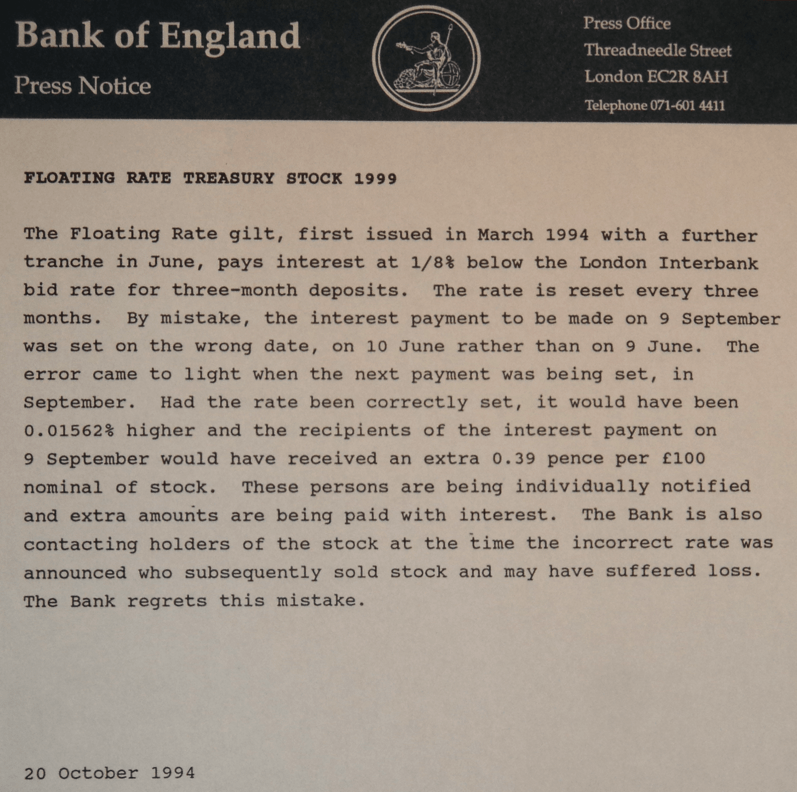

One coupon payment was mis-calculated. Bank of England, 20 Oct 1994:

The Floating Rate gilt, first issued in March 1994 with a further tranche in June, pays interest at 1/8% below the London Interbank bid rate for three-month deposits. The rate is reset every three months. By mistake, the interest payment to be made on 9 September was set on the wrong date, on 10 June rather than on 9 June. The error came to light when the next payment was being set, in September. Had the rate been correctly set, it would have been 0.01562% higher and the recipients of the interest payment on 9 September would have received an extra 0.39 pence per £100 nominal of stock. These persons are being individually notified and extra amounts are being paid with interest. The Bank is also contacting holders of the stock at the time the incorrect rate was announced who subsequently sold stock and may have suffered loss. The Bank regrets this mistake.

Nominal size was £2½bn+£2bn = £4½bn; error was 0.39 pence per £100; so the under-payment totalled £175,500.

The used fixing of Libid was a private fixing, and done only when needed, so it is not clear how the BoE could have known the value of this private fixing on a date on which it was not done. Three-month GBP Libor dropped 1.563bp between the 9th and 10th: perhaps this was used, with a small error added to hide the mechanism (perhaps, cunningly, an error chosen such that it was removed by rounding). Moral: needless complexity is needless.

| Maturity | Cpn | First settle date |

First coupon date |

Orig. term |

Formal name | ISIN, FIGI |

|---|---|---|---|---|---|---|

| 10 July 2001 | Libid−⅛% | 27 June 1996 | 08 Oct 1996 | 5.04 | Floating Rate Treasury Stock 2001 | GB0009997551 BBG0005LCMZ7 |

| 11 Mar 1999 | Libid−⅛% | 31 Mar 1994 | 09 June 1994 | 4.95 | Floating Rate Treasury Stock 1999 | GB0008880139 BBG0004HCW03 |

Sterling money-markets were and are Act/365, and gilt accrual and yield conventions were then Act/365. So we assume that a year has 365 days. Also assume that the 91-day T-Bill discount rate was d. We want to know the breakeven, at which the +50bp precisely offsets the use of a discount rate as a simple yield.

Temporarily assume that each coupon period was 91 days.

Then the simple yield was (1/(1 − d×91/365) − 1)×365/91, which is to equal d+½%.

In Mathematica (.nb, .pdf) NSolve[d + 1/200 == (1/(1 − d×91/365) − 1)×365/91 && d > −0.1 && d < 4, d] returns 13.9138%, consistent with Wormell’s “13·914 per cent”.

Except that the Bank of England said “interest payable half-yearly”, and Belchamber said “semi-annual payment”.

So instead d should be converted to a simple yield of half-year term, assumed to be 182½ days.

And NSolve[d + 1/200 == ((1 − d×91/365)^(−182.5/91) − 1)×365/182.5 && d > −0.1 && d < 4, d] returns 11.3328%.

Alternatively assuming a year of 365¼ days and an average coupon period of 182⅝ days, which are not the usual £ convention, gives 11.2405%.

So it seems that Wormell’s “13·914 per cent” is too high by more than 2½%. Please could others check my reasoning and calculations, and let me know of agreement or reasoned disagreement. Thank you.

In mid-Feb 2016 Jeremy Wormell was informed of this criticism. He said that he might reply (and presumably might not).

The Bank of England Quarterly Bulletin, December 1981, p474:

Three Treasury Variable Rate Stocks (TVRS) have been issued: in May 1977 (to mature in November 1981), July 1977 (maturing in June 1982); and January 1979 (March 1983). Each was for £400 million with interest payable half-yearly, at an annual rate ½% above the daily average of the rate of discount on 91-day Treasury bills over a previous six-month period.

Errors of punctuation and maturity date—the Bank was sloppier then! The correct maturity is confirmed by the BoE QB, June 1983, p178: “the authorities … were committed to buying (at prices of their own choosing) whatever amounts of Variable Rate Treasury Stock 1983 (whose maturity date was 24 May) were offered to them.”

Wormell (1985), pp107–108:

There appear to be six reasons for the failure of the experiment. … Fifth, the ½ per cent margin over the Treasury bill discount rate become worth less, as a proportion of the rate, as interest rates rose: ½ per cent over a 7 per cent rate is very different from ½ per cent over 14 per cent. Finally, the return was based on the discount rate on Treasury bills and not the yield. The difference absorbed the ½ per cent margin when the discount rate on bills reached 13·914 per cent.

Belchamber (March 1988), p73:

Interest was paid semi-annually at the average of the weekly three-month Treasury bill rate over the period from the preceding ex-dividend date to the ex-dividend date prior to the payment plus a margin of 50 basis points in yield.

There were three issues in the late 1970s of £400m each. They were redeemable in 1981, 1982, and 1983 with maturities at issue of four, five, and six years respectively. These issues were not ultimately successful. The coupon structure was fully mismatched. A three-month rate was used to determine a semi-annual payment of a weekly refixing basis. This complexity made analysis virtually impossible and acted as a deterent to investors. No such issues currently exist.

| Maturity | First settle date |

Orig. term |

Formal name | Implied ISIN |

|---|---|---|---|---|

| 24 May 1983 | 26 Jan 1979 | 4.33 | Variable Rate Treasury Stock 1983 | GB0090485623 |

| 15 June 1982 | 01 July 1977 | 4.96 | Variable Rate Treasury Stock 1982 | GB0090393843 |

| 17 Nov 1981 | 27 May 1977 | 4.47 | Variable Rate Treasury Stock 1981 | GB0090341180 |

— Julian D. A. Wiseman

London, February 2016 (and later updates)

www.jdawiseman.com

| Main index | Top | About author |

{kind=link}