![]()

| Main index | Financial Markets index | About author |

![]()

Julian D. A. Wiseman

Abstract: On 17th December 2008 the DMO published a wide-ranging consultation asking about other means of distributing gilts. Later that month this author sent Methods for Distributing Gilts: A Reply, after which the author was asked to present this reply at the DMO. The slides of this presentation, delivered Friday 6th February 2009, are available in PDF form, and in HTML below.

Publication history: presented on 6th February 2009 at the United Kingdom Debt Management Office, and then published at jdawiseman.com. Usual disclaimer and copyright terms apply.

Contents: Slides; Auctionettes; Call options; Discussion.

Better Auctions

|

The price is how ‘good’?

|

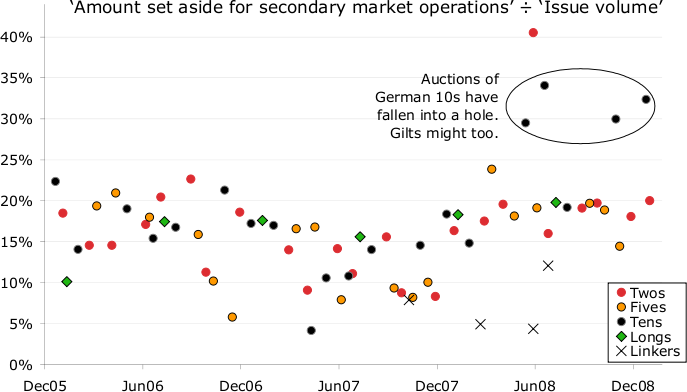

Germany: unsold proportion

Chart showing ‘Amount set aside for secondary market operations’ ÷ ‘Issue volume’. Observe that German 10s have fallen into a hole—and gilts might too. |

Three Possibilities

|

Failure of auction mechanism

|

Why failure to find price?

|

How fix?

|

How to fix, as an auction?

|

What to reveal about bids?

|

What to reveal about bids?

|

Soft pressure

|

A GEMM’s Strategy

|

A GEMM’s Strategy

|

Details: Deemed Bids

|

Details: Minimum Price

|

Details: Squeezes

|

Auctionettes: Q & A‘Q’ first; ‘A’ second. |

Selling calls on long gilts

|

Details: Underlying

|

Details: Expiry

|

Details: Strikes

|

Details: Structure

|

Scale

|

Options as Taps

|

Options: Q & A‘Q’ first; ‘A’ second. |

In discussion it became clear that two matters had not been stated explicitly.

If the DMO so desired, the first few auctionettes could be smaller than the standard size. For example, auctionettes could be £30mn for the first, £70mn for the second, and £100mn subsequently. However, this complexity ought to be redundant, as the £100mn was chosen to be a size in which a GEMM might ordinarily make a price. Also note that some care should be taken in drafting the rule that determines which auctionette(s) are shrunk by the size of the retail non-competitive allotment.

Whilst a program of selling options on a particular gilt is happening, and hence there are options outstanding with that particular gilt as underlying, there can still be auction(ette)s of that gilt. Indeed, the fact that GEMMs own such options would be likely to improve demand—reduction in tail risk helping the bidders. Even a GEMM that doesn’t own any options would know that others do, and that their ownership reduces the likelihood of market misbehaviour.

— Julian D. A. Wiseman |

| Main index | Top | About author |